By: Alex Turgeon, President at Valere

TL;DR: 3 Key Takeaways

- Software companies that fail to commit fully to either aggressive AI-native growth or true margin discipline face accelerating multiple compression with no clear path out.

- AI is not just a product feature; it is the primary mechanism through which Path One and Path Two targets become achievable by multiplying output per employee and enabling outcome-based business models.

- The shift from seat-based licensing to service as software is already redefining how enterprise buyers purchase, and companies that internalize it early will compound significant advantages over those that wait.

There is a reckoning underway in software, and it is moving faster than most boards want to acknowledge.

Public markets have already weighed in. After peaking at median EV/Revenue multiples of 18.6x in 2021, the sector compressed to 6.1x in 2023 before stabilizing somewhere between 7.0 and 7.4x today. That stabilization is deceptive. I may come off like Michael Burry, but underneath it, a real stratification is happening. Companies commanding 9x-plus multiples are pulling away from those stuck well below the median, unable to grow fast enough to justify a premium and unable to cut deep enough to earn a fortress valuation.

The comfortable middle is gone. What replaces it is a decision every software CEO, board member, and investor needs to make now, and make clearly.

The Adjusted EBITDA Reckoning

For the better part of a decade, software companies got very good at one thing: looking profitable without actually being profitable. Non-GAAP operating margins, adjusted EBITDA, and free cash flow figures quietly excluded the dilutive cost of stock-based compensation. These became the industry’s preferred language, and investors were willing to play along.

That era is over.

The SBC Problem Is Getting Harder to Hide

In 2026, stock-based compensation as a percentage of revenue remains eye-watering across the sector. SoundHound AI sits at 48%. Snowflake at 35%. Rubrik at 26%. Cloudflare at 21%. Treating SBC as the real expense it is — a genuine transfer of value from shareholders to employees — makes much of the sector’s apparent profitability disappear. Nvidia’s recent decision to stop excluding SBC from its adjusted operating expenses signals where the rest of the industry is headed: toward full transparency, whether companies choose it or not.

The implication is uncomfortable but straightforward. If your growth is slowing and your true margins are still deeply negative, you have neither a growth story nor an efficiency story. The Rule of 40 is no longer a premium signal. It is a floor requirement for institutional relevance. Bessemer’s move to a “Rule of X” framework applies a 2 to 3x multiplier to revenue growth over margin improvement. Growth endurance has already declined from 80% to 65% across the sector, and the market is pricing that in.

Grow fast or earn real money. There is no third option.

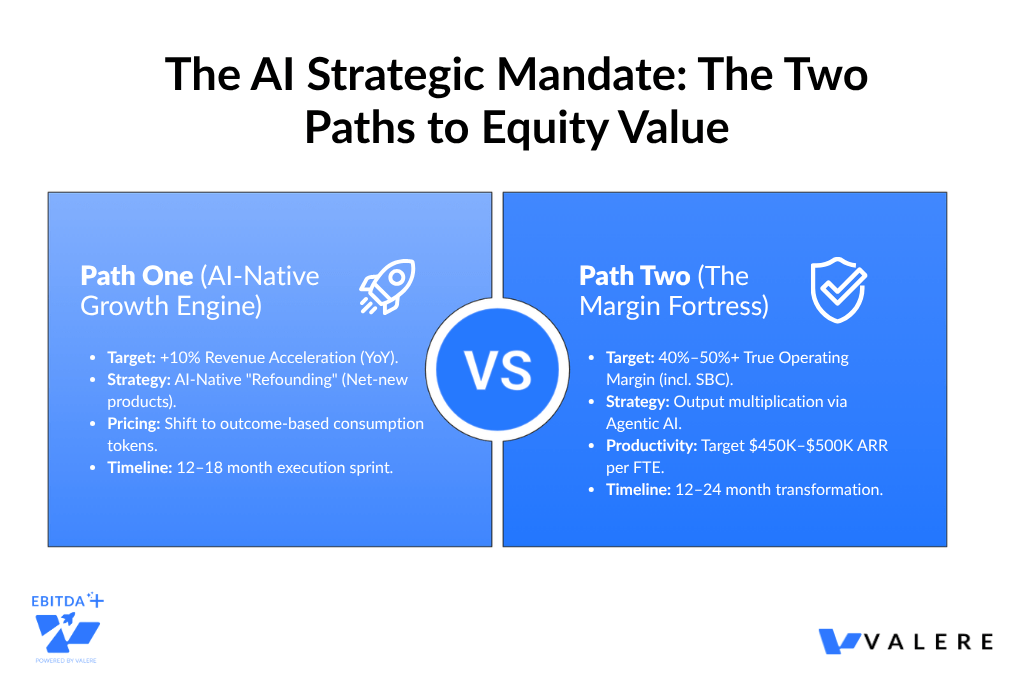

Two Paths, No Middle Ground

The market evidence keeps pointing to the same conclusion. Durable equity value creation in software now flows through one of two mandates.

- Path One: Accelerate revenue growth by 10 or more percentage points year-over-year through genuinely new AI-native products, within 12 to 18 months.

- Path Two: Rebuild to 40 to 50%+ true operating margins, inclusive of stock-based compensation, within 12 to 24 months.

These paths are not mutually exclusive in theory. In practice, they are. Management bandwidth, capital allocation, and organizational energy cannot stretch across both without producing half-measures on each.

Why the Middle Is the Most Dangerous Place to Be

The companies most at risk right now are not the ones boldly pursuing either path. They are the ones pursuing a diluted version of each, convinced that moderate growth and improving-but-not-true margins represent a defensible position.

They do not. McKinsey’s research reinforces the danger. Companies that prioritized margin between 2021 and 2023 while passing on investable growth left meaningful enterprise value on the table. A 6-point reinvestment in growth, even at lower efficiency, could have yielded a 9% EV uplift. The takeaway is not that Path Two is wrong. A company choosing Path Two should be genuinely unable to pursue Path One — not just reluctant about it.

The rise of AI-native micro-teams makes the urgency more acute. Small, highly capable teams are competing in niche markets with a fraction of the overhead of established players. For a mid-sized company carrying high personnel costs and a legacy tech stack, trimming headcount by 8%, launching a cautious AI feature, and publishing an aspirational margin target is not a strategy. It is a slow compression story.

Path One: The AI-Native Growth Engine

The first thing to understand about Path One is what it is not.It is not adding a chatbot to your pricing page, not a press release about your AI roadmap, and not a copilot bolted onto an existing product.

Path One is a refounding. It means new products capable of moving your total growth rate by 10 percentage points within 12 months. The organization has to rebuild around those products so that when product-market fit arrives, you can actually capitalize on it.

What the Market Data Says

The numbers on AI-native companies make the urgency hard to ignore. AI-native startups reach $1M ARR 30% faster than top-quartile traditional SaaS benchmarks. They reach $30M ARR five times faster — in roughly 20 months versus the traditional 100. Implementation timelines run 10x shorter. Costs in some verticals run 20x lower. These are structural advantages, not incremental ones. They come from data flywheels, organizational agility, and architectures built for the agentic era from the start.

Salesforce’s Agentforce is the clearest incumbent-side reference point. By the end of fiscal 2026, the platform reached approximately $800M in ARR, up 169% year-over-year. It processed 19 trillion tokens and delivered 2.4 billion agentic work units across 29,000 signed deals. That is not a feature launch. That is a business model transformation — from seat-based licensing to outcome-based consumption, priced in tokens and aligned to workflows enterprise buyers actually care about now.

A Real Example of Path One Done Right

I have seen this distinction play out directly. One enterprise software platform in the Microsoft licensing space had already invested in a chatbot prototype. It ran on fragile automation that fell apart under real enterprise queries. The temptation was to iterate. The right answer was to start over.

Rebuilt from the ground up on an enterprise-grade AWS architecture and reoriented around enterprise buyer needs, the product improved chatbot accuracy by 50%. It unlocked a $100M-plus revenue customer segment the platform had previously been unable to reach. That is Path One done properly — a transformation that changes who can buy from you and at what scale.

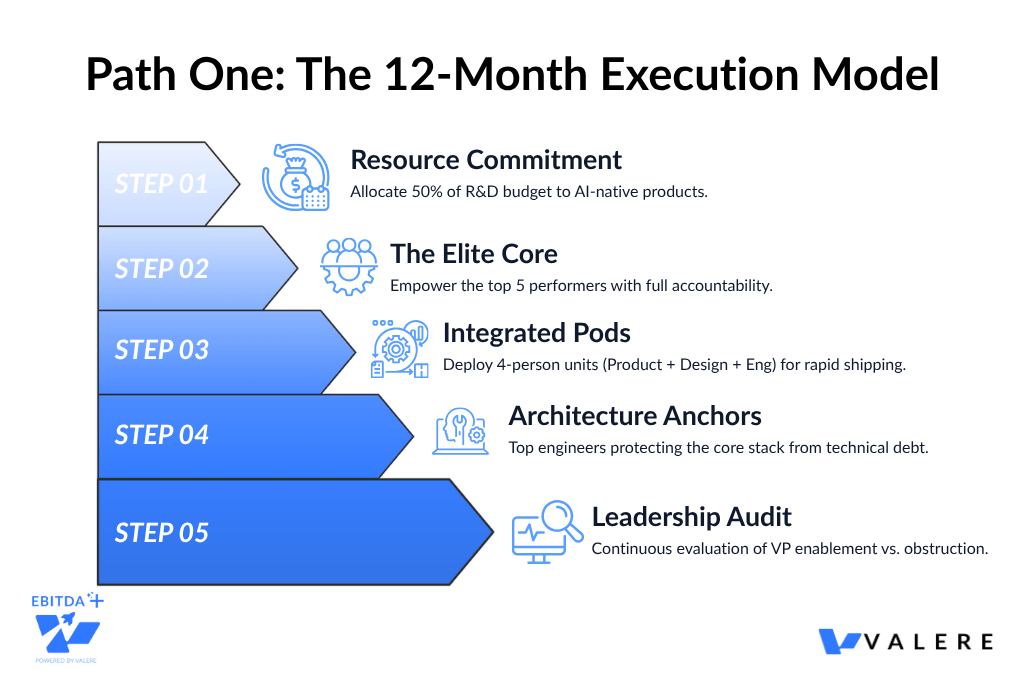

How to Structure the Execution

The companies that pull this off treat it as a 12-month sprint with a small, trusted team at the center. Find the five people in your organization, regardless of title, who will outperform every expectation over the next year. Give them real scope and accountability. Watch closely to see which of your VPs enables them and which quietly gets in the way. Those observations will tell you most of what you need to know about which leaders to keep.

On R&D, allocate 50% of budget to net-new AI products. Organize work in four-person pods that integrate design, product, and engineering into a single shipping unit. This consistently produces better results than anything built across traditional functional silos. Keep your best engineers anchored in the central architecture. Spreading top engineering talent across discovery pods fragments the stack and creates technical debt that quietly buries early progress.

Rethink the Business Model Too

The business model has to evolve alongside the product. Seat-based pricing will erode because your customers’ most visible source of AI savings is labor efficiency. Seats are exactly where they will look to cut first. The new growth is in tokens, consumption pricing, outcome-based contracts, and machine-driven workflows. If an AI agent cannot autonomously consume and pay for your product, you are not yet set up for Path One.

Path Two: The Margin Fortress

For companies where top-line reacceleration is not a realistic option, Path Two is not a consolation prize. Executed with discipline, it produces businesses with the durability, pricing power, and cash generation to compound through the next cycle.

But it is routinely misunderstood. An 8 to 10% reduction in force is not Path Two. That is the weak form — trimming the edges while leaving the machine intact. The strong form is rebuilding the machine.

What the Targets Actually Require

Reaching 40 to 50%+ true operating margins requires moving spend ratios significantly across every function. The 2025 median for private SaaS companies shows Sales and Marketing consuming 37 to 47% of revenue and G&A consuming 19 to 24%. Path Two targets S&M below 20%, R&D below 15%, and G&A below 10%. Gross margins need to push above 85% and net revenue retention above 115%. You cannot get there through incremental adjustments. It requires a coherent redesign across the full organization.

AI is the primary mechanism that makes the required output-per-employee ratios achievable without gutting the business.

Output Multiplication, Not Cost Cutting

A construction technology company we worked with needed to scale outbound email marketing but could not justify the headcount to do it manually. Rather than hiring, we deployed AI to capture and codify successful messaging patterns from the team’s existing work. We then built an orchestration layer to execute those patterns autonomously at scale. Agents now manage dynamic personalization, reply routing, and compliance monitoring across 210 to 300 inboxes. They handle over 250,000 contacts without adding a single person to a three-person team.

That is not a cost-cutting story. It is an output-multiplication story, and it is the mechanism through which Path Two margin targets become achievable without hollowing out organizational capacity.

Unlocking Revenue Capacity

A government contracting firm we work with was losing significant sales capacity to manual opportunity research. Teams spent hours scanning procurement databases and cross-referencing agency budgets, often chasing stale leads. We built agents to continuously scan SAM.gov, USAspending, and Navy budget databases around the clock. The agents score opportunities in real time and generate alerts when a match surfaces. Manual search time dropped by 80%. The team now identifies high-value opportunities 30 to 90 days earlier than before. A lean sales team produces what a much larger capture department used to.

Path Two is not only about cutting costs. It is about making every dollar of retained cost dramatically more productive.

The PE Playbook as a Blueprint

The private equity playbook, historically dismissed by VC-backed founders as too efficiency-obsessed, turns out to be the right model for Path Two. Firms like Thoma Bravo and Vista Equity Partners have spent decades proving that software can run as a precision instrument. Vista’s portfolio migrations from fragmented legacy platforms to unified modern alternatives consistently produce 50 to 80% reductions in licensing and infrastructure costs. Zero-based budgeting delivers 15 to 20% OpEx reductions. Value-based pricing anchored in workflow ownership and switching costs adds 3 to 5% margin expansion almost immediately. Broadcom under Hock Tan remains the starkest public-market proof that the strong form is achievable, even before AI entered the picture.

AI Raises the Output Ceiling

Top operators now describe engineers managing 20 to 30 agents simultaneously. Order-of-magnitude productivity gains are becoming the expectation, not the exception. Path Two companies that invest aggressively in AI tooling can ship more while reducing headcount dependency. Median ARR per FTE at the $50M to $100M band sits around $200 to $240K today. Top-quartile is $300K. With agentic tooling deployed properly, $450 to $500K is achievable within 18 months.

Protecting the Revenue Base

Customer retention is the other half of the margin equation that too few Path Two plans take seriously enough. An automotive dealer intelligence platform we partner with was spending disproportionate CS capacity on reactive churn management — identifying at-risk accounts too late to intervene. We surfaced the early warning signs of dealer churn that existed as tribal knowledge but had never been captured in any system. We then built automated monitoring to track platform usage patterns in real time and recalculate account health scores continuously.

The result: 15% of CS bandwidth freed from manual auditing, proactive intervention triggered 30 to 60 days before traditional churn indicators appeared, and a 20% reduction in early-stage churn. Margin expansion is partly about cost structure. It is equally about protecting the revenue base those margins depend on.

Know Where Your Moat Actually Is

Be clear-eyed about which moats are weakening. Data alone is usually not the defensible position it once was. Integrations are easier to reproduce. Workflow and UI advantages erode when agents move across systems. Migration is getting easier, not harder. The companies that succeed at Path Two know exactly where their pricing power lives, and they protect it while cutting everywhere else.

Service as Software: The Business Model Shift Underneath Everything

Running through both paths is a fundamental change in how software is bought, sold, and valued. It affects nearly every strategic decision on the table right now.

The seat-based SaaS model rested on a simple premise: software delivers value to the humans who use it, so you charge per human. That premise is breaking down. AI agents are increasingly doing the work — handling customer interactions, processing transactions, generating outputs, and orchestrating workflows. Agents do not have seats. They consume tokens.

This is the shift to service as software: outcomes delivered autonomously, priced by consumption, and valued by the work completed rather than the license held.

What This Looks Like in Practice

One of the clearest examples is a content quality platform whose value proposition depended entirely on human teams manually reviewing image and text annotations against a dense, 50-page rulebook. The work was genuinely valuable. The delivery mechanism was not scalable — every unit of growth required a proportional unit of labor.

We built an AI-powered logic bridge that maps the full rulebook into precise JSON logic. The system now evaluates any annotation submission, generates a quality score, and produces a complete audit trail in a single API call. A fragmented, labor-intensive review process became a scalable, outcome-based software service. Rule application, exception handling, and quality assessment all now run through the software itself.

That is what service as software looks like in practice. Not AI-assisted humans working faster — AI performing the work directly, with humans setting the parameters and reviewing the outputs.

The Downstream Implications

The ripple effects touch every part of the business. Customer success teams built around user adoption metrics become less relevant when the user is an agent. Sales motions built around named-user licensing need rethinking. Gross margin profiles shift as compute becomes a larger share of COGS. The pricing model itself has to rebuild from first principles.

Companies that internalize this shift early will compound their advantages. Those that treat it as something to address later will find it arriving as a crisis.

The Question Every Board Should Be Asking

The honest framing of our work at Valere is this: we close the gap between AI strategy and AI value actually delivered. That turns out to be a different problem for nearly every organization we work with.

What We See Consistently

What tends to be consistent is the shape of the challenge. Path One companies usually carry more organizational inertia than they realize and have less time than they think. Path Two companies often underestimate how much of their cost structure sits behind management layers that have never been asked to justify their existence. And companies on both paths almost always have more usable knowledge locked inside their own teams — in undocumented processes, tribal sales wisdom, and implicit instincts — than they have ever captured in any system.

The AI capability is rarely the limiting factor. Organizational knowledge, process clarity, and the willingness to redesign around outcomes rather than activities — that is where most of the real work happens. The client wins we have seen came not from sophisticated models, but from understanding the problem clearly before writing a line of code.

Choose a Direction and Execute With Conviction

That brings it back to the question that should sit on the first page of the next board deck: are we growing 10 points faster through AI-native products, or rebuilding to 40 to 50% true margins?

If the answer is some version of a little of both, expect the pressure to continue. If the answer is a clear path with a clear timeline and clear ownership, the refounding moment is available.

A fragile chatbot became an enterprise-grade platform that opened a new customer segment. A three-person team took on the output of a full department. A manual review service became a deterministic, API-delivered software outcome. A reactive CS function became a proactive one that catches churn a quarter before it happens. A lean sales team started identifying high-value government contracts weeks before the competition.

None of these required dramatically more capital or entirely different people. They required a clear-eyed choice about which path to take, the right architecture for getting there, and an honest commitment to treating AI as a structural redesign rather than a feature update.

The divide in software is not temporary. It reflects a permanent shift in how software is built, delivered, and valued. The companies that emerge on the right side of it will be the ones that chose a direction and executed it with conviction.

Work With Valere

Choosing between Path One and Path Two is consequential enough to get right. Valere works with private equity sponsors and portfolio companies to close the gap between AI strategy and AI value actually delivered — whether that means rebuilding a product to unlock a new customer segment, deploying agents to multiply the output of a lean team, or redesigning a cost structure around what AI now makes possible.

If you are evaluating AI maturity across existing assets, preparing a portco for transformation, or determining which path a new acquisition target should pursue, Valere brings the expertise, platform, and operating experience to move from diagnosis to results.

- A clear-eyed assessment of where your current AI investments produce real structural advantage and where they generate activity without compounding value

- A path from disconnected pilots and cautious feature launches to an operating model built around AI-native products, outcome-based pricing, and agents that scale output without scaling headcount

- A value creation roadmap aligned to the specific mandate of the business — whether that is 10 points of growth acceleration or 40%+ true margins — with the architecture, team structure, and execution plan to get there

Start the conversation: https://www.valere.io/

Frequently Asked Questions

How do mid-market software companies typically start with AI implementation?

Most mid-market software teams start by identifying where they are losing the most productive capacity: manual review processes, repetitive outbound, reactive customer success workflows. The companies that see the most durable results begin with knowledge capture work before building any automation. The underlying judgment in those workflows is usually more complex than it appears. Starting with agentic tooling before codifying the decision logic tends to produce agents that perform well in demos and poorly in production.

What does an AI readiness assessment typically include for a software company?

A thorough readiness assessment covers four things: the current cost and output structure of the workflows most likely to be automated; the state of existing data and knowledge documentation; the organizational capacity to absorb change without disrupting the core business; and an honest look at which path is actually executable given the company’s current position. Most assessments that skip the last question produce technically valid recommendations that never get implemented.

How do you evaluate whether to pursue revenue acceleration or margin improvement first?

The answer usually comes down to growth endurance. If net revenue retention is above 115% and the market genuinely supports 10+ percentage points of growth acceleration through AI-native products within 18 months, Path One tends to be the higher-value choice. If growth has already decelerated and NRR is under 110%, Path Two is typically more honest. Most companies assume they can pursue both simultaneously. The evidence suggests that committing to one path produces significantly better outcomes than a divided effort.

What is the difference between AI strategy and AI execution?

AI strategy identifies which workflows and business model changes represent the highest-value targets for transformation. AI execution gets those changes into production without disrupting the business while they are being built. Most of the gap between companies that generate meaningful AI ROI and those that do not comes down to execution: the knowledge capture work, the architecture decisions, and the organizational redesign. Strategy without execution infrastructure tends to produce well-reasoned slide decks and very little else.

How do PE-backed software companies typically approach AI transformation differently than VC-backed ones?

PE-backed software companies tend to move faster on the margin side because the path to exit is more clearly defined and the tolerance for extended investment cycles is lower. The firms with the strongest outcomes apply PE-style discipline to cost structure while simultaneously investing in the agent infrastructure that allows remaining headcount to operate at significantly higher output. The combination of zero-based budgeting and aggressive token spend per engineer tends to produce better results than either approach on its own.